Following two years of poor capital performance for real estate, impacted by the sharp rise in interest rates in Q4 2022 and increased competition from other asset classes (notably cash & gilts), the market has now reached an inflection point where UK real estate is once again offering an attractive investment opportunity for charities and endowments.

The UK property market posted its first positive quarterly total return in Q4 2024 since Spring 2022, driven by increased investment activity. This pick-up in performance and positive investor sentiment has continued into 2025 despite global markets reeling from the impact of US-led trade tariffs and their impact on equity, currency and bond markets. UK property is relatively well insulated, providing resilient, recurring income, and with the benefit of values already re-based. With the Bank of England cutting interest rates to 4.25% in May and with further cuts anticipated over the coming year, we expect this to lead to a widening of property’s risk premium, a further positive indicator for future property performance.

Global investor sentiment for real estate indicates that the UK remains the most sought-after European destination for overseas capital due to relative fair pricing and ongoing rental growth, pointing to further improvements in investment volumes for 2025.

Looking forward, the Investment Property Forum* (IPF) forecasts total returns from property of 8.0% annualised over the next 5 years; however, sector positioning remains critical to relative performance – with industrial, residential and retail park assets set to outperform. *IPF UK Consensus Forecasts (Winter 2025) Report

Reasons to be Positive on Property:

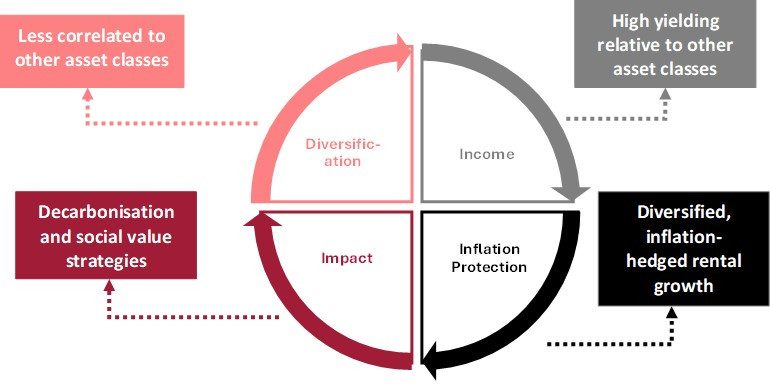

Given the above macro conditions, what are the key attributes of an allocation to real estate within a diversified investment portfolio for charities and endowments?

1. Diversification: Property acts as a strong diversifier within multi-asset portfolios. Over the longer term, bonds and equities have little correlation with real estate, whilst also offering different return characteristics. Diversification is an attribute that has become increasingly important, given the growing concentration risk within investment portfolios and increased volatility experienced so far in 2025.

2. Income: Property continues to produce a high nominal yield compared with other asset classes of *5.3% (as at March 2025), with further potential for reversion given property’s ability to capture income growth (from lettings, lease renewals, rent reviews etc..) unlike Gilts. Property’s income return dominates its overall total return and makes up over 80% over the last 40 years. While capital values fluctuate through market cycles, income remains consistently positive and largely predictable, which is a key attraction for charities and endowments, that, for many, rely on their investment returns to support their mission. *Source: MSCI UK Property Monthly Index, March 2025

3. Inflation Protection: Although not a perfect hedge, property has provided reasonably strong inflation protection over the long run, with all property producing a total real return of 4.6% pa over the last 30 years. Looking forward, real total returns from property are expected to be above 5% ‘real’ (according to the IPF Consensus estimates); therefore, proving attractive returns for charities and endowments with CPI+ 3-4% targets. Property can also offer above inflation rental growth, if allocated to the right sectors of the market. In recent years, industrial and residential sectors, have benefited from favourable supply demand characteristics, driving ‘real’ (above inflation) rental growth, whilst assets with indexed linked leases can also provide some inflation protection to portfolios. *Source: MSCI UK Property Annual Index, 2024

4. Impact: Property is a real asset, influenced by social, economic and demographic change, providing the opportunity to deliver genuine impact. The built environment contributes significantly to carbon emissions, so reducing this through decarbonisation strategies and improving the efficiency of property assets can deliver genuine positive impact, as well as better financial returns*. More recently this has included the move towards social impact strategies, with investors having the ability to give back to local communities in and around their assets, through social value initiatives. *UK Sustainability Index Results to Q4 2024

With H1 2025 signaling the start of a new cycle, we believe it is an opportune time for charities and endowments to consider a re-allocation to real estate. While inflation is expected to continue its downward trend, it is likely to stay higher than in the previous decade. Inflation will remain a headwind for charity and endowment portfolios to continue their grant-making and spending, alongside maintaining their investment portfolio value in real terms. With real estate presenting inflation hedging characteristics, through a combination of above inflation rental growth and index linked leases, we believe the asset class can provide a stable cornerstone for an investment portfolio, whilst also offering true diversification against equity and fixed income returns.

If you would like to discuss your real estate requirements with one of our team

Please get in touch by clicking the link below.